Mastering Business Debt Consolidation: Strategies for Financial Freedom

Business debt can accumulate quickly, whether from expansion efforts, unexpected expenses, or economic fluctuations. For many entrepreneurs, managing multiple loans, credit lines, and payments becomes overwhelming, leading to cash flow issues and hindered growth.

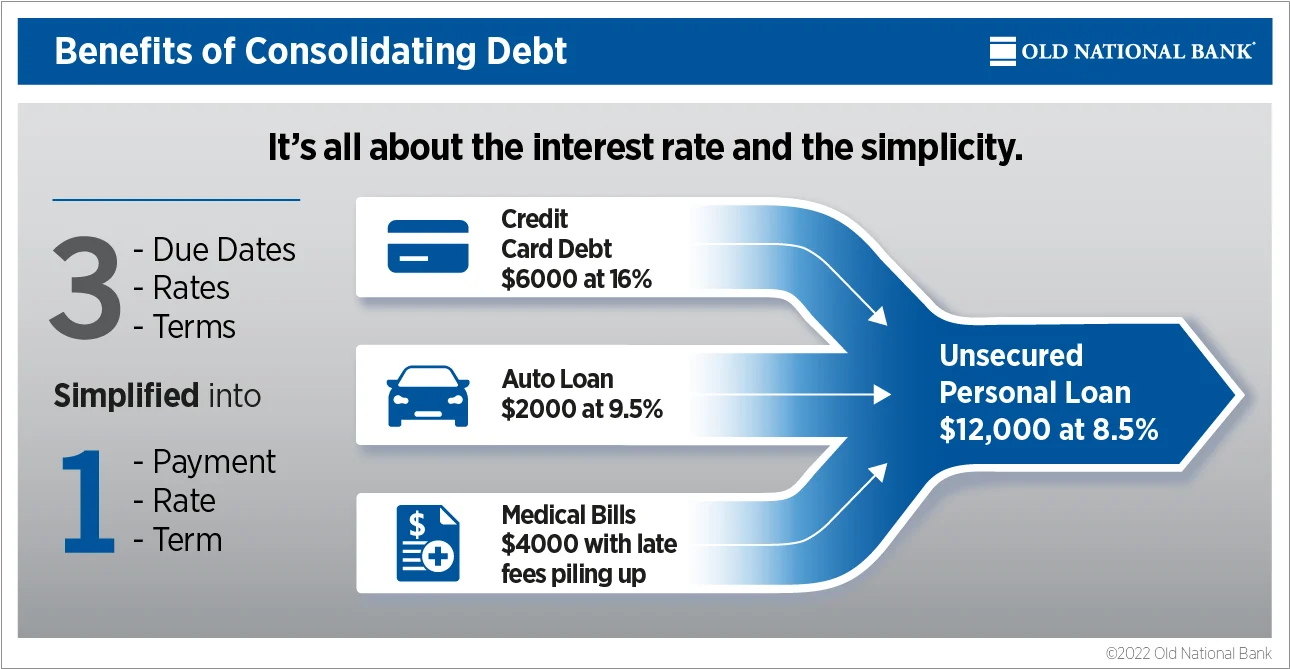

Debt consolidation emerges as a practical solution, allowing business owners to streamline their obligations into a more manageable structure. This approach not only simplifies finances but also potentially reduces costs over time through lower interest rates and extended repayment terms.

At its essence, business debt consolidation involves merging multiple debts into one loan or payment plan. Beyond the basics, partnering with experienced advisors can make a significant difference. Firms like STG Liberty, with their specialized Business Advantage Consulting Program, provide tailored support to navigate consolidation effectively and position businesses for sustainable growth.

Why Business Debt Consolidation Matters

Key Benefits of Business Debt Consolidation

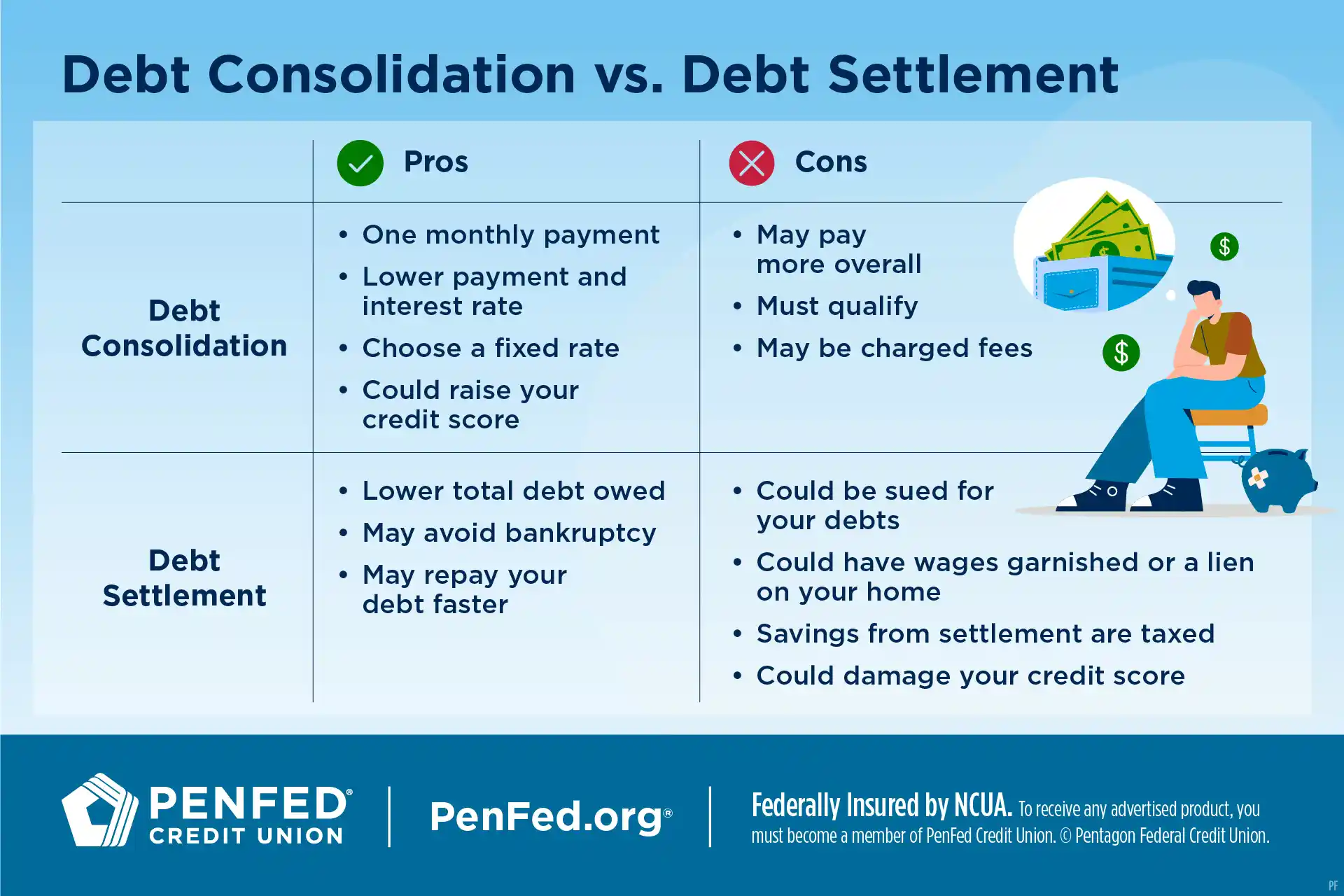

Debt Consolidation vs. Debt Settlement

Key Differences:

Combines multiple debts into one new loan with potentially better terms. Preserves credit relationships and improves credit scores over time with consistent payments.

Negotiates with creditors to accept less than full amount owed. Can severely damage credit and may result in legal consequences or tax liabilities on forgiven debt.

For most businesses, consolidation is the preferred strategy as it maintains creditworthiness while improving financial management.

Types of Business Debt Consolidation Options

Common Sources of Business Debt

| Debt Source | Description | Typical Rates |

|---|---|---|

| Term Loans | Fixed amounts repaid over time for equipment, real estate, or expansion | 7-15% APR |

| Business Credit Cards | Revolving credit for short-term needs with high interest if balances carry | 15-25% APR |

| Lines of Credit | Flexible borrowing up to limit for fluctuating expenses and cash flow gaps | 8-18% APR |

| Merchant Cash Advances | Quick funds based on future sales, extremely costly for businesses | 40-150% APR |

| Equipment Financing | Asset-specific loans for machinery, vehicles, or technology purchases | 6-12% APR |

How to Qualify for Business Debt Consolidation

Step-by-Step Guide to Consolidating Business Debt

Risks and Considerations in Debt Consolidation

Alternatives to Debt Consolidation

Common Pitfalls and How to Avoid Them

The Role of Professional Advisors in Debt Consolidation

DIY approaches work for some, but complex debt scenarios benefit significantly from expert guidance. Professional advisors analyze finances, negotiate favorable terms, and identify optimal consolidation strategies that align with long-term business goals.

STG Liberty stands out in this arena. Specializing in business financing and debt solutions, they offer personalized strategies for consolidation, growth, and cash flow optimization through their comprehensive approach.

STG Liberty Business Advantage Consulting Program Benefits:

- Comprehensive financial analysis and debt assessment

- Strategic lender matching and term negotiation

- Cash flow optimization and budget restructuring

- Fractional CFO expertise for complex situations

- Ongoing support throughout consolidation process

- Long-term growth planning and funding access strategies

Real Success Story:

A retail business struggling with multiple high-interest loans consulted STG Liberty. Through their Business Advantage Consulting Program, they secured a consolidation loan at a reduced rate, freeing 20% more cash for inventory—boosting sales by 15% within a year while maintaining healthy debt service coverage.

In a landscape where business debt continues to rise and default risks remain elevated, partnering with experienced advisors like STG Liberty can mean the difference between financial struggle and sustainable success.