Getting a Business Line of Credit: A Comprehensive Guide

In today's dynamic economic landscape, businesses of all sizes often need flexible financing options to manage cash flow, seize opportunities, and navigate unexpected challenges. A business line of credit stands out as one of the most versatile tools available, allowing entrepreneurs to access funds on demand without the rigidity of traditional loans.

Unlike term loans where you receive a lump sum upfront and repay in fixed installments, a line of credit functions like a credit card for your business. You only pay interest on the amount you actually use, and as you repay, the available credit replenishes for future draws. This flexibility makes it ideal for covering short-term expenses like inventory purchases, payroll during slow seasons, or emergency repairs.

Beyond the basics, partnering with experienced advisors can streamline the process and uncover hidden opportunities. For instance, firms like STG Liberty specialize in guiding business owners through complex funding scenarios via their Business Advantage Consulting Program, which tailors strategies to individual needs and ensures optimal credit utilization.

Why Business Lines of Credit Matter

What is a Business Line of Credit?

Key Characteristics:

- •Revolving Nature: Funds available repeatedly as you repay, within your credit limit

- •Interest Calculation: Variable rates based on prime rate plus lender's margin

- •Draw Period: Initial 12-24 months for drawing funds, followed by repayment phase

- •Fees: Potential origination, annual maintenance, or draw fees vary by provider

Example: With a $50,000 limit, you could draw $10,000 for marketing, repay it, then access $15,000 for equipment—all without reapplying.

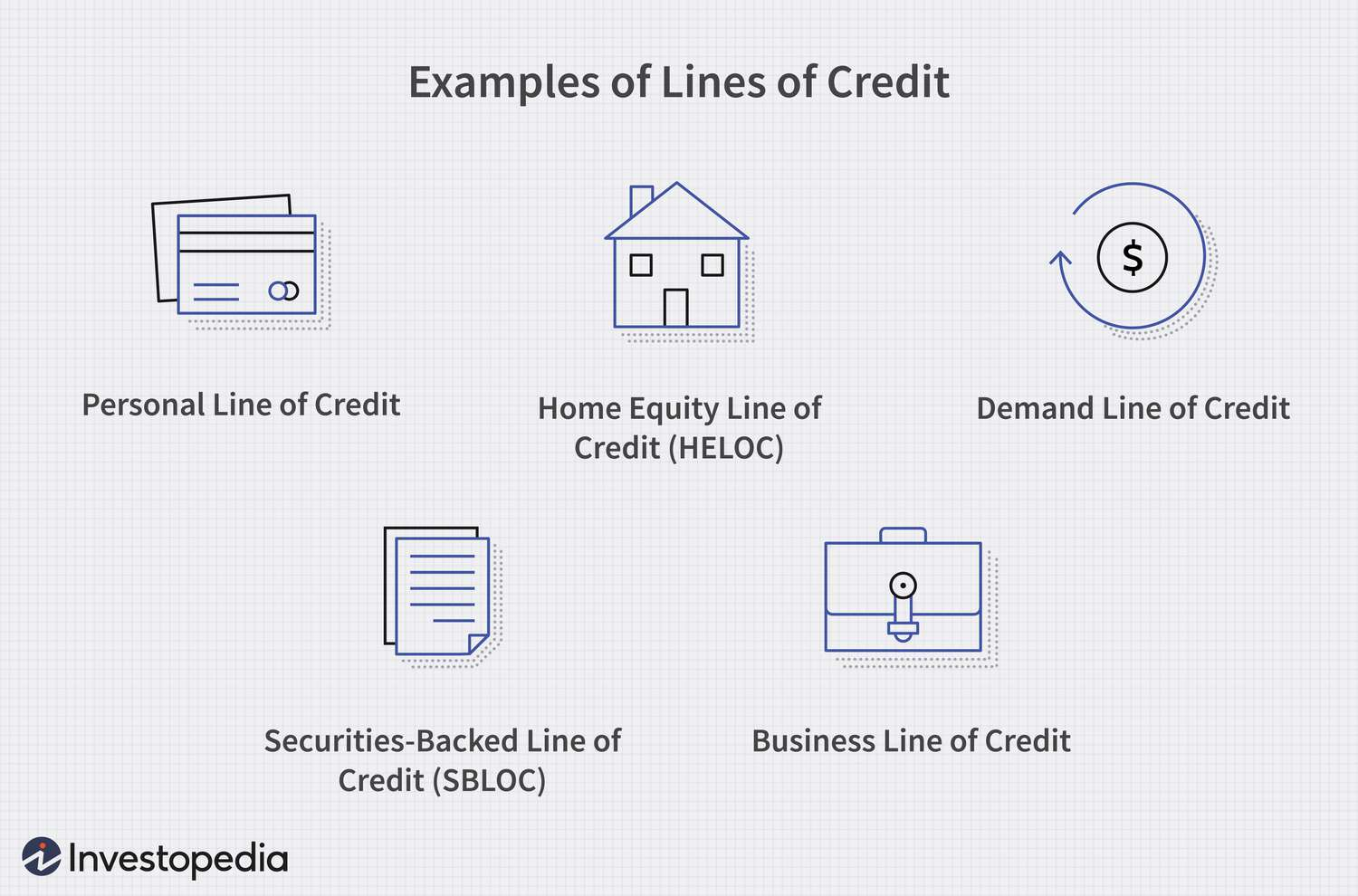

Types of Business Lines of Credit

Eligibility Requirements for Business Lines of Credit

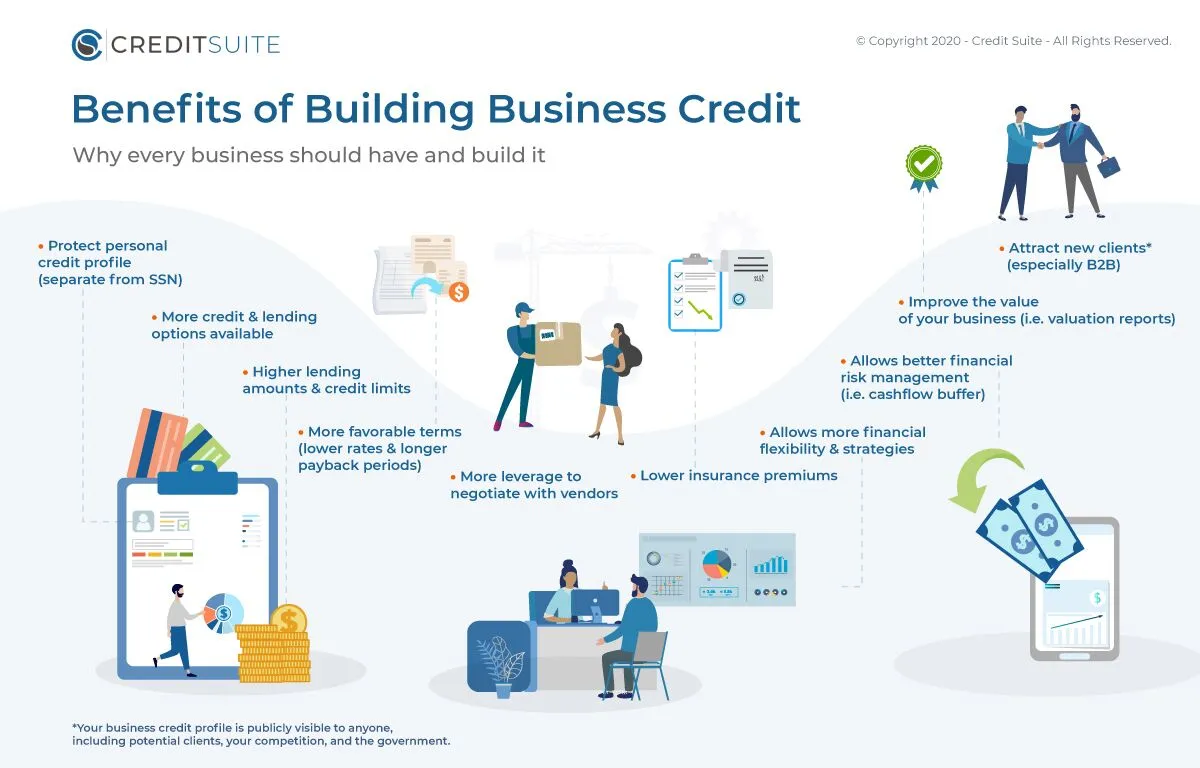

Key Benefits of Business Lines of Credit

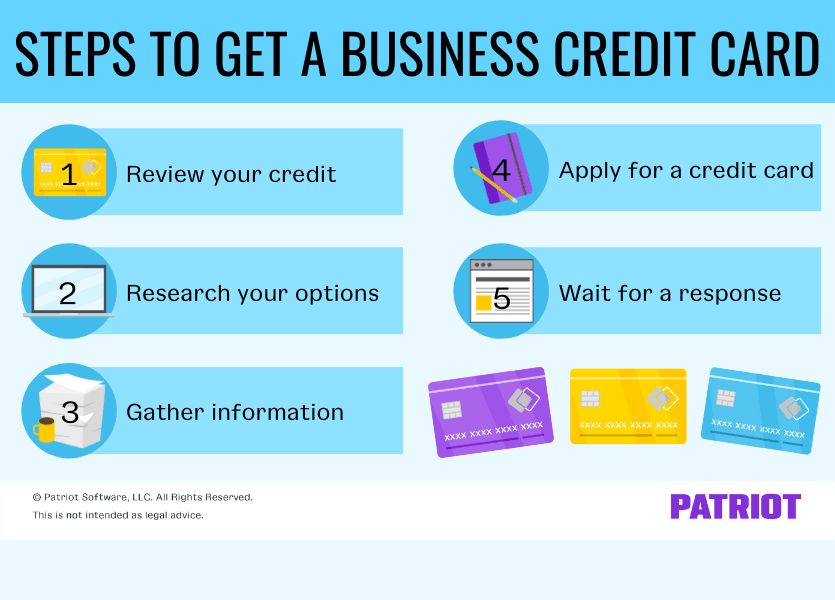

Step-by-Step Application Process

Tips for Increasing Your Approval Odds

Pro Tips for Success:

- Shop around but space out inquiries to avoid score impacts

- Consider co-signers if credit is weak

- Apply during stable economic periods for better lender flexibility

- Use rejection feedback to improve and reapply

Alternatives to Business Lines of Credit

Common Pitfalls and How to Avoid Them

Why Use STG Liberty for Advisory Services

Navigating financing complexities demands expertise, which is why partnering with a trusted advisor like STG Liberty is invaluable. Specializing in business loans, debt consolidation, and growth strategies, STG Liberty empowers owners with tailored solutions.

Their Business Advantage Consulting Program stands out by offering comprehensive assessments, credit optimization, and lender matching. This program helps identify the best lines of credit, negotiate favorable terms, and avoid common pitfalls—ultimately saving time and money.

STG Liberty Business Advantage Consulting Program Benefits:

- Comprehensive financial health evaluation and credit optimization

- Strategic lender matching and term negotiation

- Assistance with securing working capital and equipment financing

- Support for startups with limited revenue history

- Access to competitive rates through extensive lender network

- Guidance on strategic credit utilization for sustainable growth

In an era where financial decisions impact long-term success, STG Liberty's guidance ensures businesses not only obtain credit but use it strategically. Many clients report smoother processes and significantly better outcomes thanks to this comprehensive approach.