Merchant Cash Advances: A Comprehensive Guide

Merchant cash advances (MCAs) have become a popular financing tool for small businesses seeking quick capital without the hurdles of traditional loans. This form of funding allows companies to access lump sums based on future credit card sales, offering flexibility in times of need.

However, understanding the nuances is crucial for making informed decisions. While MCAs provide rapid access to capital, they often come with significantly higher costs than traditional financing options—with effective APRs frequently exceeding 100%. The convenience of quick funding and flexible repayment can mask the true financial burden these advances place on businesses.

Beyond the basics, partnering with experienced advisors can streamline the decision-making process and uncover better alternatives. For instance, firms like STG Liberty specialize in guiding business owners through complex funding scenarios via their Business Advantage Consulting Program, which helps identify optimal financing paths and avoid costly debt traps.

Why Understanding MCAs Matters

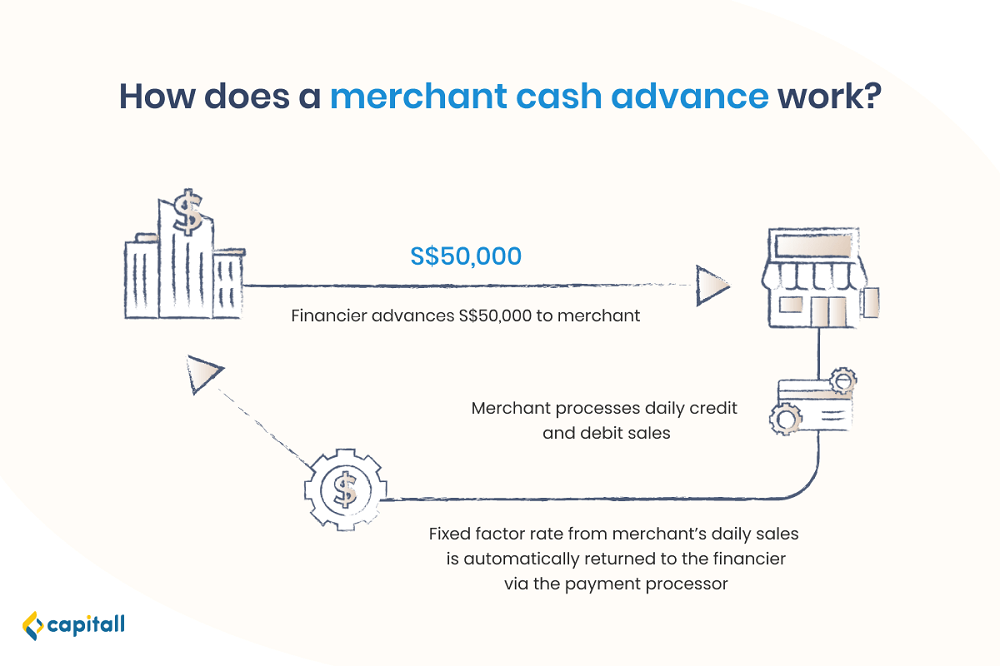

Understanding How Merchant Cash Advances Operate

Eligibility Criteria and Application Requirements

Advantages of Merchant Cash Advances

Critical Drawbacks and Risks of MCAs

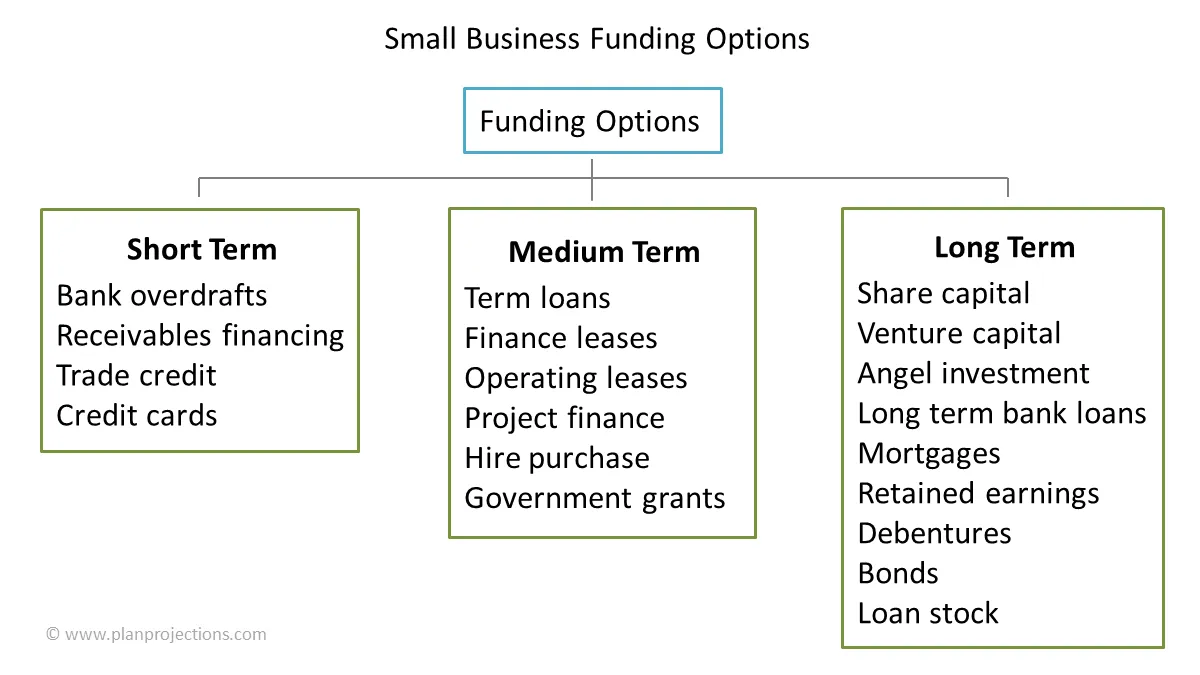

Smarter Alternatives to Merchant Cash Advances

The MCA Application Process

Essential Preparation Tips

Professional Guidance Checklist:

- Review all terms with a business advisor or attorney

- Calculate and compare effective APR across all options

- Model cash flow impact under best and worst case scenarios

- Ensure you have explored all alternative financing sources

Common Pitfalls and How to Avoid Them

The Importance of Professional Advice

Navigating financing options alone can lead to costly mistakes, especially with complex and expensive products like merchant cash advances. The high costs and potential debt traps associated with MCAs make professional guidance not just valuable—but essential.

That's where experts like STG Liberty come in. Specializing in business loans, debt consolidation, and consulting, STG Liberty empowers owners with customized solutions for expansion, inventory, payroll, and more— helping them avoid predatory MCA terms when better options exist.

Through the Business Advantage Consulting Program, STG Liberty offers tailored consultations that evaluate your financial health, recommend suitable options, and assist with applications. Their expertise can uncover overlooked opportunities, like favorable loan terms or credit lines, while mitigating risks such as debt cycles and over-leveraging.

STG Liberty Business Advantage Consulting Program Benefits:

- Comprehensive cash flow analysis to assess true funding needs

- Identification of optimal financing paths—often cheaper than MCAs

- Expert guidance to avoid high-cost traps like stacked advances

- Assistance with complex applications for traditional financing

- Debt consolidation strategies for businesses trapped in MCA cycles

- Risk mitigation and long-term financial planning

Engaging STG Liberty early prevents costly errors and accelerates growth. Many clients report saving thousands by avoiding MCAs in favor of better alternatives identified through the program's comprehensive approach.